Plaquette indemnisation des Catastrophes Naturelles en France - CCR

PUBLICATIONS

Natural disasters compensation scheme

Principles and operation

12/08/2022

NATURAL DISASTER COVERAGE IS COMPULSORY in all property insurance policies. Almost all victims of natural disasters therefore benefit from the coverage.

France is one of the very few countries with a system that guarantees all its citizens adequate compensation, in the event of loss and/or damage caused by a natural phenomenon.

This document summarises the system's bases and principles and how it works.

BASES AND PRINCIPLES

The natural disaster compensation scheme was created by the Law of 13 July 1982. It was introduced to make up for the inadequate cover of natural disasters, for which, until then, only very low levels of insurance were provided.

It is based on paragraph 12 of the preamble of the Constitution of 27 October 1946, which states: "The Nation declares all French citizens to be equal and united in solidarity when faced with loss resulting from natural disasters."

The scheme's design is comparable to a building:

1. it has been skilfully designed, based on a detailed plan – legislator's specifications;

2. it rests on solid foundations – solidarity and responsibility;

3. it has been built on solid cornerstone – public-private partnership;

4. it has solid pillars – insurance and State-backed reinsurance;

5. it has a keystone that gives it stability and longevity – State guarantee.

1. Plan: design sustainable, widespread and affordable cover without neglecting prevention

The legislator had to design a system on the following specifications:

•provide widespread, effective cover (private individuals, businesses and local authorities) for all perils;

•mutual-based insurance scheme providing compensation for property loss and/or damage caused by natural disasters at affordable rates;

•successfully combine solidarity and responsibility by incorporating prevention tools (Risk Prevention Plans or R.P.P.) in the system;

•optimise efficiency by combining skills from both the public and private sectors;

•guarantee solvency and sustainability.

The legislator created a coherent compensation scheme, all parts of which are inextricably linked in effectively serving the public interest.

2. Foundations: solidarity and responsibility

These two fully complementary values are the scheme's founding principles:

•Solidarity takes the form of the same additional-premium insurance rates (set by the government) applying to all those covered by the scheme.

These rates currently stand at:

•12% of the premium of the basic insurance policy covering property other than motor vehicles,

•6% of premiums for fire and theft insurance (or, failing this, 0.50% of the property insurance premium) for motorised land vehicles.

These rates thus, enshrine the solidarity principle in the natural disaster scheme, irrespective of the level of risk exposure, guaranteeing cover for everyone at affordable prices – it being specified that natural disaster cover is compulsory in all property and casualty insurance policies.

The Scheme's solidarity is also provided by state-backed reinsurance, enabling insurance portfolios to be mutualised at national level and which has the State guarantee (see below).

•Responsibility is ensured by deductibles and risk prevention plans.

The Law of 13 July 1982 established a compensation scheme including compulsory deductibles together with a prevention plan (Risk Exposure Plans, which today have become Risk Prevention Plans).

These links between compensation and prevention have been strengthened by a sliding scale that adjusts the deductibles applying to communes that do not have Risk Prevention Plans, to encourage them to introduce such plans.

Accordingly, since 1 January 2001, in communes without Risk Prevention Plans, it has been possible to adjust deductibles after two government declarations of disaster concerning the same type of peril (except for motor insurance policies).

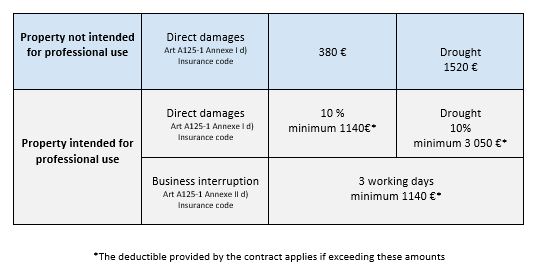

Minimum compulsory deductibles

They are set by the State, are compulsory and cannot be “bought back”. Since 1 January 2001, they have been set as follows:

Sliding scale for adjusting deductibles:

1-2 declarations of disaster: Basic deductible

3 declarations of disaster: Basic deductible X 2

4 declarations of disaster: Basic deductible X 3

5 declarations of disaster: Basic deductible X 4

3. Cornerstone: public-private partnership

The two preconditions that must be met to trigger the compensation scheme clearly illustrate this partnership:

•Condition of a public nature: a government decree declaring a disaster must be published in the Official Journal.

•Condition of a private nature: the lost and/or damaged property must be covered by a property and casualty insurance policy (fire, theft, flooding, etc.).

Moreover, a causality link must exist between the declared natural disaster and the loss and/or damage sustained.

More generally, the public-private partnership is established through the pillars and cornerstone that constitute the compensation scheme's inextricable components.

4. Building pillars: insurance and state-backed reinsurance

Strengths of insurance:

It mobilises true risk-sector professionals. The insurers and their loss adjusters are in charge of:

•distributing and establishing mutual-based statutory cover, through their insurance policies (compulsory cover);

•collecting monies (statutory additional premiums);

•quickly calculating and indemnifying those having suffered losses in accordance with the regulatory conditions.

•Thanks to such use of the insurance sector, the natural disaster compensation scheme is a local, responsive and efficient service, that is governed by law and serves the general interest.

Advantages of state-backed reinsurance:

State-backed reinsurance proposed to insurers by Caisse Centrale de Réassurance (CCR) is a second vector for ensuring the scheme's mutual basis and a guarantee of stability.

It is a general interest initiative since CCR is mainly tasked with:

•reinsuring any insurer so requesting within the legal framework, irrespective of its book of business;

•providing mutual-based reinsurance, at national level, of all risks by reinsuring the various insurers' books of business;

•creating robust and sustainable reinsurance cover, by avoiding too large a transfer of risks to the reinsurer and, indirectly, to the State.

5. Keystone: State guarantee

Natural disaster risks can engender major disasters and substantial losses, the cost of which cannot be borne solely by the insurance and reinsurance markets.

In order to avoid any failure of the system, the legislator has provided for State intervention as a last resort. Accordingly, the State guarantee is extended to CCR, to enable it to fulfil its general-interest mission, as mentioned above. This guarantee is therefore the final constituent part of the building, that represents the natural disaster compensation scheme.

However, CCR does not have a monopoly on natural disaster reinsurance.

The natural disaster scheme is therefore comparable to a solid and well-designed building which is able to provide compensation commensurate with the extent of losses:

•losses resulting from average events are borne jointly by insurance and state-backed reinsurance;

•the same applies for larger events or losses, but with a greater proportion of losses borne by state-backed reinsurance;

•finally, losses caused by major events are borne by all the scheme's players: insurance, reinsurance and the State.

The scheme thus, compensates the population without State intervention, except in exceptional circumstances where losses exceed the scheme's funding abilities.

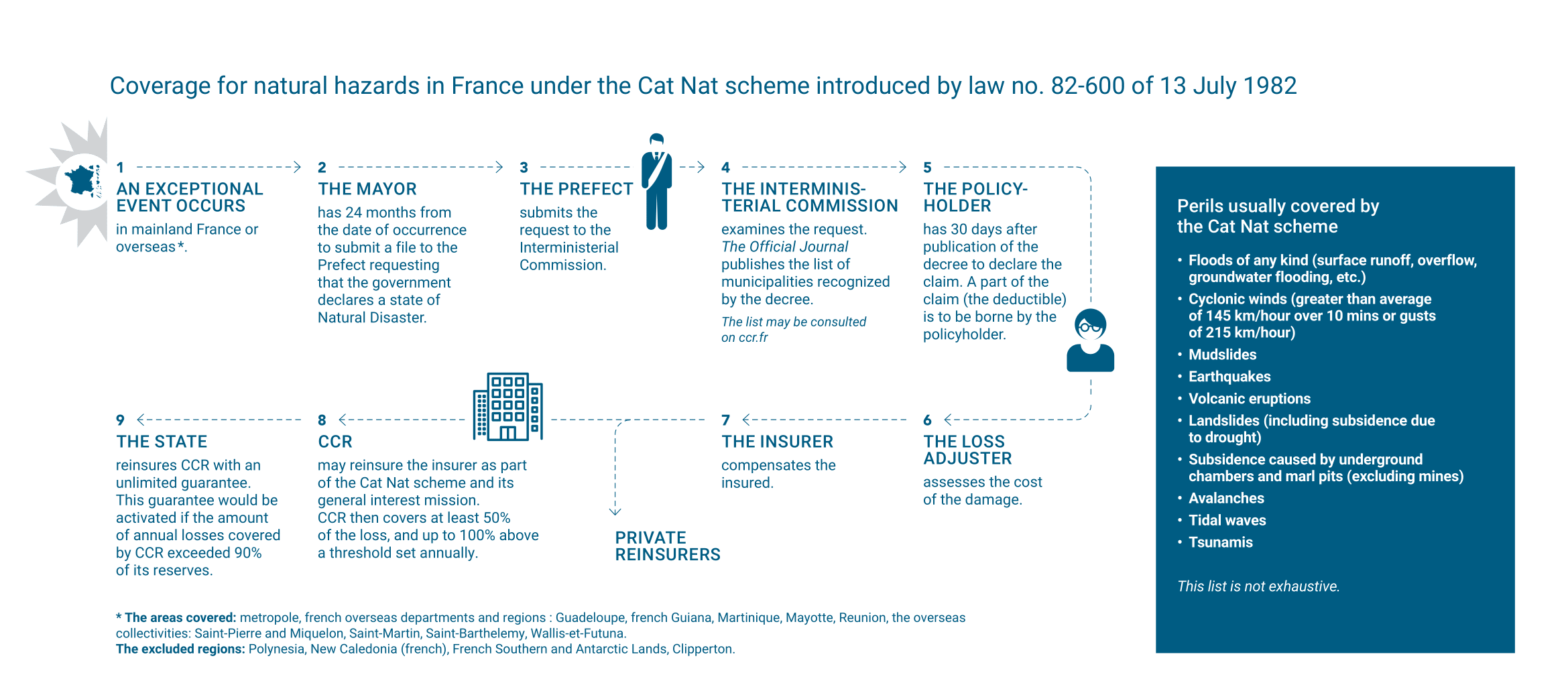

HOW THE SCHEME WORKS

Government declaration of natural disaster

1. Mayor's role

The mayor initiates the request that the government declare a natural disaster, by sending the prefect a form, containing the following information:

•date, time and phenomenon identification;

•type of property damaged;

•number of previous government declarations of disaster;

•any prevention measures taken.

Any request made by a commune twenty-four months after the beginning of the natural event is refused.

2. Prefect's role

The prefect prepares a file containing:

•a detailed report established by it's departments;

•the mayor's files;

•the list and location of applicant communes;

•a technical report on the phenomenon's nature and intensity, prepared by a competent department;

•any other document (photos, press cuttings, etc.) that can be used to analyse the phenomenon.

3. Interministerial Commission

The interministerial commission has no real legal existence. It prepares the ministers' decisions concerning the declaration of natural disaster.

It meets once a month or so (except in exceptional circumstances).

It comprises the following ministrys' representatives:

•Ministry of the Interior: Civil Security and Crisis Management Directorate (examines requests, convenes and chairs the commission, signatory to disaster declaration decrees);

•Ministry for Overseas Departments and Territories: Overseas Departments and Territories Directorate (present only when overseas departments and/or territories are concerned - signatory to disaster declaration decrees);

•Ministry of Economic Affairs and Finance: Treasury and Budget Directorate (signatories of disaster declaration decrees);

•Ministry of Ecology, Sustainable Development and Energy: Risk Prevention Directorate (technical adviser to the commission – not a signatory to disaster declaration decrees).

CCR fulfils the role of secretariat.

The Commission's assessment criteria are as follows:

•for floods: frequency of recurrence;

•for standard landslides: phenomenon's natural nature, volume, suddenness, unpredictability, etc.;

•for subsidence and rehydration: soil moisture and type;

•for avalanches: phenomenon's cause, location and age of affected buildings;

•for earthquakes: magnitude, macroseismic survey results.

The main reasons why the Commission refuses requests are as follows:

•the event's exceptional intensity is unproven (most frequent);

•the peril is outside the scope of the Law of 1982;

•there is a prevention failure (a very rare case);

•the prefectoral file is incomplete (deferment).

A deferred or refused request may be re-examined, if the prefecture submits additional information.

State guarantee: insurance and reinsurance roles

Main characteristics of the "natural disasters" legal guarantee

The guarantee's introduction was facilitated by property and casualty insurance's very high penetration rate in France.

It is not a true insurance scheme but a compensation scheme based on a public-private partnership that uses the insurance industry's networks and mechanisms together with substantial government support.

The key standard insurance elements are out of insurers' control:

•decision to insure the risk (compulsory extension of cover);

•government declaration of disaster;

•definition of covered perils;

•cover conditions (standard wordings);

•rate setting;

•deductibles.

System's scope

The Law of 13 July 1982 provides a list neither of covered perils nor of excluded perils. Article 1 of this law only describes what is considered as being the effects of a natural disaster.

Definition: "uninsurable direct material loss and/or damage the determining cause of which was the exceptional intensity of a natural element."

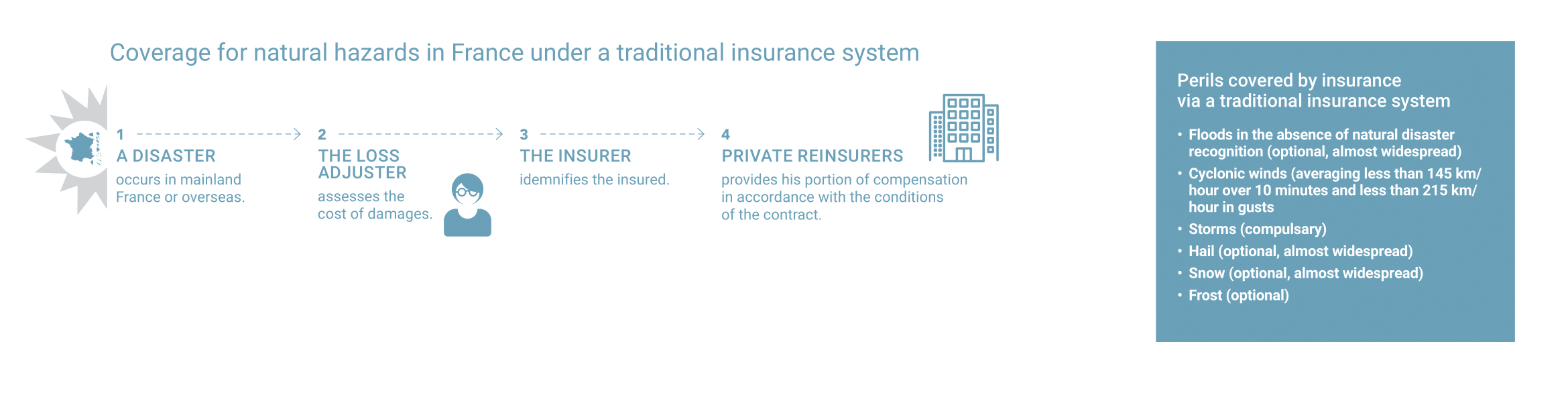

1. Perils normally covered

Perils coming within the scope of application of the Law of 1982:

•floods (run-off flooding, overflow, rising of water table level, dam burst caused by a natural phenomenon);

•mudslides;

•earthquakes;

•landslides (including subsidence);

•subsidence caused by underground chambers and marl pits (excluding mines);

•tsunamis;

•avalanches;

•cyclonic winds (greater than average of 145 km/hour over 10 mins or gusts of 215 km/hour).

This list is not exhaustive.

2. Perils excluded in principle

Because they can be insured, the following perils are considered to be outside the scope of "natural disaster" cover:

•storms (except for high-amplitude cyclonic winds);

•hail;

•snow;

•frost.

They are covered by insurance, which justifies their exclusion from the statutory natural disaster scheme.

CCR'S ROLE

CCR is the state-backed reinsurer of the natural disaster scheme. It does not have a monopoly on natural disaster reinsurance. It fulfils a public interest role within the framework of the scheme.

The State guarantee was granted to CCR by the Law of 13 July 1982, that created the natural disaster compensation scheme, of which the guarantee constitutes a key component.

Reasons for its intervention

•It is in exchange for the insurers' obligation to provide cover.

•The State guarantee enables CCR to offer insurers –who are obliged to provide their policyholders with natural-disaster cover, without being able to limit their liability–, reinsurance comprising unlimited cover.

•By being authorised to reinsure natural disasters with the State guarantee, CCR enables the State to ensure, that the scheme for compensating victims of natural disasters, remains solvent.

CCR's missions

•Offer robust and sustainable reinsurance cover.

•Ensure that the State guarantee applies only in the event of exceptional losses.

•Thus, ensure the longevity of the natural disaster compensation scheme.