2020 CCR group's financial position - CCR

NEWS

2020 CCR group's financial position

04/09/2021

2020 financial position

The 2020 financial statements (CCR standalone and Group consolidated) were approved for publication by CCR’s Board of Directors on April 7, 2021. After the meeting, the Chairman of the Board, Pierre Blayau, said:

“In last year’s singularly difficult Covid-19 environment, the CCR Group powerfully demonstrated

the quality of its business model.

CCR fulfilled its corporate mission by deploying a mechanism to support supplier credit, which plays an important role in fueling the domestic economy, and by providing protection against the financial impacts of natural disasters.

CCR Re continued to grow its business, raised new debt and improved its solvency ratio, while also preserving its income despite the losses associated with Covid-19 and the Beirut explosion. It held firm to the trajectory set in the strategic plan, and I would like to congratulate the Chief Executive Officer and his teams for their performance.”

The CCR Group had €1,866 million in consolidated gross written premium and €90 million

in consolidated net income in 2020.

CCR – Public reinsurance

In an environment shaped by the Covid-19 pandemic, the French government called on CCR

to provide reinsurance cover for the portfolios of domestic credit insurers through the Cap, Cap+ and Cap Relais mechanisms, adding €260 million to its gross written premium for the year.

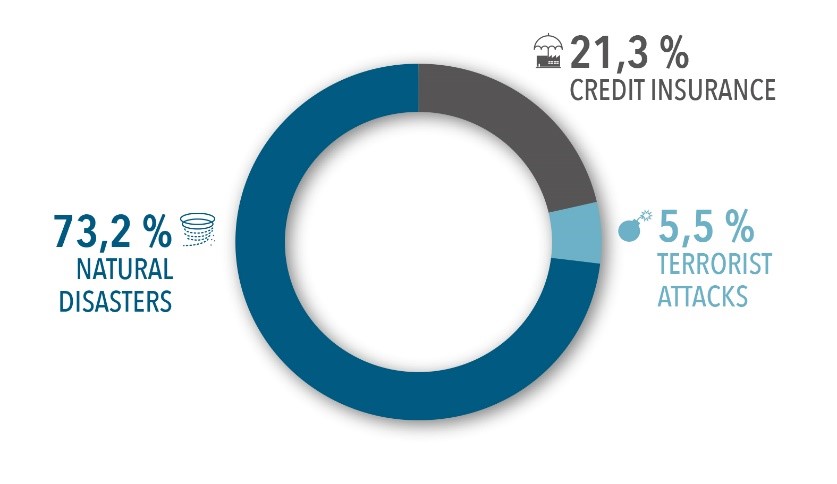

- The company’s gross written premium for 2020 came to €1,215 million, up 29% on 2019.

This amount breaks down as follows by business line:

- Natural disaster claims were high in 2020, with a major drought affecting a quarter of France

and extensive flood damage caused by storm Alex in October. In all, natural disaster losses

for the year amounted to €775 million. - CCR’s return on investment was 1.3%. The portfolio’s market value stood at €8.6 billion

at December 31, 2020, reflecting an increase of €426 million over the year. - The company’s cost ratio stood at 2.1%.

- CCR’s net income on a stand-alone basis came to €61 million.

- In 2021, CCR has sufficient capital to absorb natural disaster losses of up to €4.6 billion without drawing on the State guarantee.

(in millions of euros) |

2019R |

2020R |

|

|

|

Gross written premium |

945 |

1,215 |

Cost ratio |

2.0% |

2.1% |

Net combined ratio |

96.3% |

97.4% |

Return on investment |

1.5% |

1.3% |

Net income for the year |

67 |

61 |

Shareholders’ equity(1) and equalization reserve(2) |

4,381 |

4,269 |

- Shareholders’ equity before appropriation of income

- Equalization reserve pursuant to Articles R.343-8 and R.431-27 of the French Insurance Code

CCR Re

CCR Re’s financial statements were approved for publication by the company’s Board of Directors on March 25, 2021.

In an exceptional environment shaped by the Covid-19 pandemic and the Beirut explosion, CCR Re preserved its margins, reporting net income for the year of €18 million.

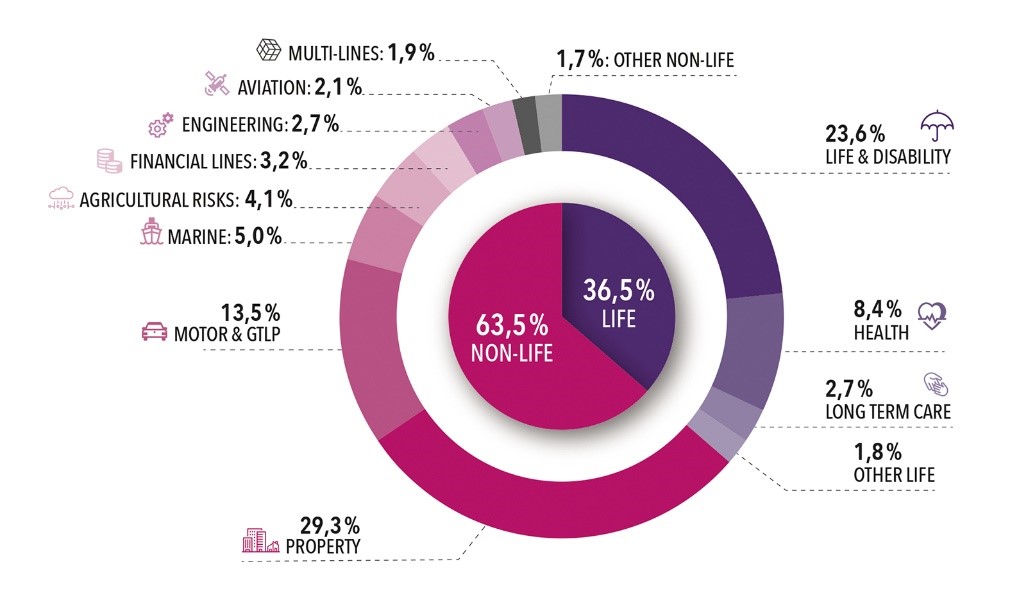

- The company’s gross written premium rose 16% to €649 million, in line with the trajectory set in the Streamline strategic plan. The business mix was as follows:

- CCR Re’s combined ratio stood at 103.2%. Life technical margin was 2.2%. Excluding

the managed impact of the Covid-19 pandemic (€49 million before and after reinsurance) and the Beirut explosion (€24 million before reinsurance and €15 million after reinsurance), underwriting margins continued to improve thanks to pricing action. - CCR Re's return on investment was 2.6%. The portfolio had a market value of €2.9 billion

at December 31, 2020, up by some €400 million (+16%) compared to the previous year-end. This increase resulted in particular from the investment of the proceeds of CCR Re’s €300 million Tier 2 subordinated notes issue in July 2020. - Cost ratio improved to 4.9%, in line with the trajectory set in the Streamline strategic plan.

- EBITER came to €39 million.

- CCR Re’s net income for the year was €18 million.

- Its solvency ratio stood at 199.2% at December 31, 2020, in the optimal [180%-220%] range defined by the risk appetite framework.

- CCR and CCR Re’s financial reports will be published on the companies’ websites on April 14.

(in millions of euros) |

2019R |

2020R |

|

||

Gross written premium |

562 |

649 |

Year-on-year change (%) |

+21% |

+16% |

Cost ratio |

5.5% |

4.9% |

Life technical margin |

5.2% |

2.2% |

Net combined ratio |

98.1% |

103.2% |

Return on investment |

2.7% |

2.6% |

EBITER |

60 |

39 |

Net income for the year |

35 |

18 |

|

||

Solvency coverage ratio (Solvency II) |

185% |

199% |

Cost ratio: ratio of management expenses net of investment expenses and net of taxes on the one hand, and written premiums gross of retrocession on the other.

Life technical margin: ratio, for life business, of the sum of technical result and interest on cash deposits on the one hand, and the total earned premiums net of retrocession on the other. 2018 technical margin pro forma.

Net combined ratio (CCR RE): ratio, for non-life business, between the net claims expense excluding variation in the equalization reserve and expenses incurred net of investment expense (including commissions) on the one hand, and net earned premiums on the other.

Net combined ratio (CCR): ratio between the net claims expense including variation in the equalization reserve and expenses incurred net of investment expense (including commissions) on the one hand, and net earned premiums on the other.

Return on investment: ratio between net investment income on the one hand, and outstanding investments on the other hand, excluding cash deposits, real estate for one use and financial expenses due to the subordinated loan.

EBITER: earnings before interest, taxes and the equalization reserve. EBITER also excludes non-recurring items.

NB:

The CCR Group’s statutory auditors have completed their audit of the financial statements. This press release contains both historical information and forward-looking statements with respect to CCR and CCR Re. Forward-looking statements contain information about future events, expectations, objectives

and performance, and are based on assumptions currently adopted by CCR and CCR Re management. Although CCR and CCR Re believe that these forward-looking statements are based on reasonable assumptions, they are not a guarantee of the future performance of CCR or CCR Re. Actual results may differ materially from the forward-looking statements as a result of risks and uncertainties. CCR and CCR Re undertake no obligation to publish updates or revisions of these forward-looking statements.

Media contacts:

Vincent Gros – General Counsel + 33 (0)1 44 35 38 36 - vgros@ccr.fr

Sophie Bodin - DGM Conseil + 33 (0)1 40 70 11 89 – s.bodin@dgm-conseil.fr